SC Ventures makes strategic investment in Algbra, establishes partnership with its UK sustainable finance platform Shoal#News

Algbra becomes first ethical FinTech to receive Authorised E-Money Institution License from the FCA#News

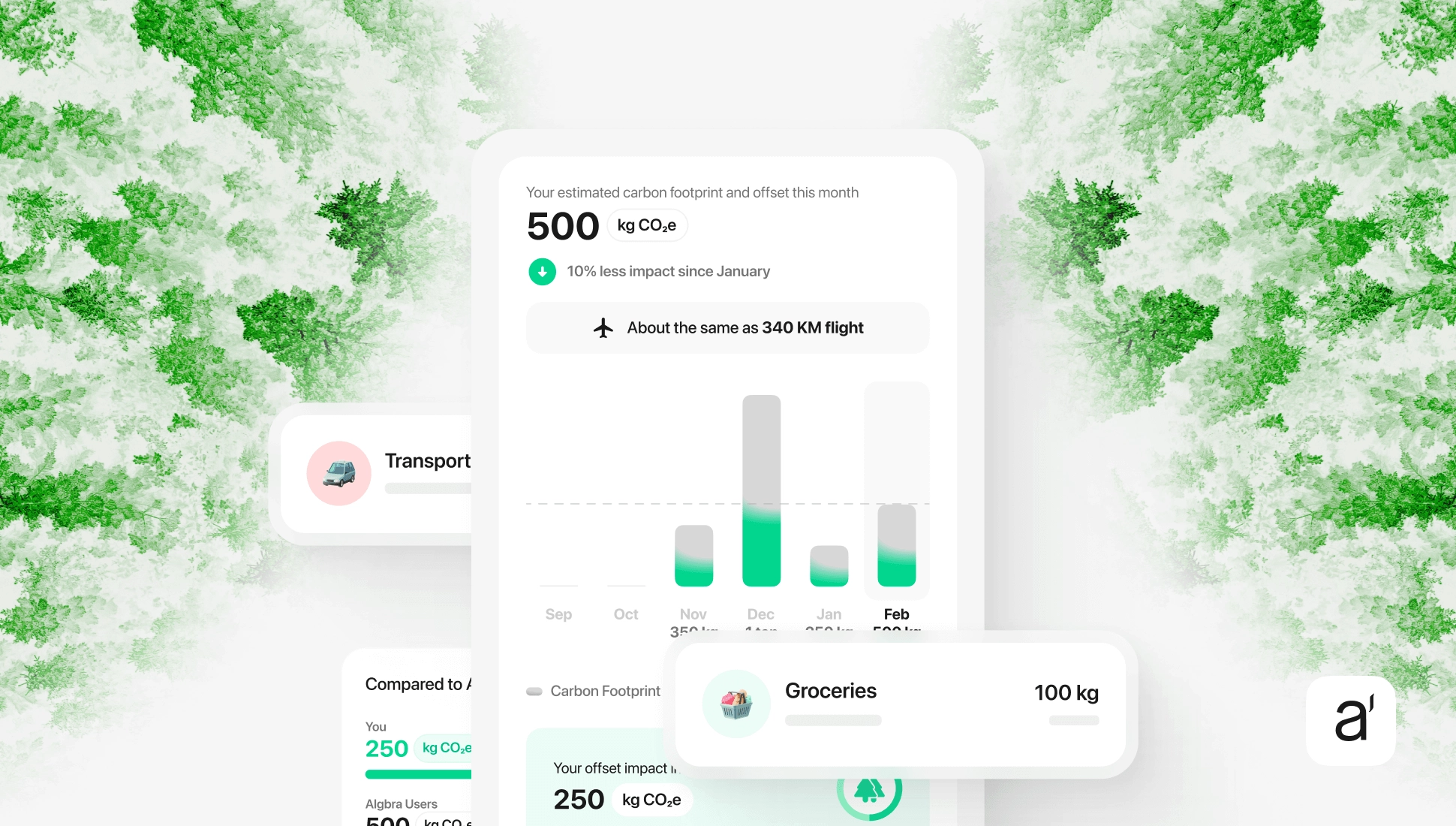

Algbra unveils its comprehensive values-focused and climate-impact fintech with strategic Mastercard partnership#News

Algbra Partners with Doconomy at COP26 to Further its Sustainability Agenda With Global Minority Communities#News

Fetch.ai Partners with Algbra, Bridging AI and Blockchain with Banking Solutions for Ethical Finance and Minority Communities#News

Former Chancellor Lord Philip Hammond – Backs Algbra’s Quest to Deliver Sustainable and Values-Based Finance#News